Notes, thoughts and observations - Compiled weekly

Growth is slowing around the globe and central banks in Canada, Australia and the Eurozone are signaling rate increases. At some point that will bleed over into the US.

Union pressure ramps up at Amazon as ALU partners with the Teamsters. Hands on labor is still in demand even though office work has been in recession for over a year.

EVs continue to drag down automotive sales and a used car price correction is underway.

The real estate market is still hot, but inventories are starting to recover to pre-pandemic levels. This will create downward pressure on prices but don’t expect a major correction. The real relief will come from more starter homes being built.

A different kind of M&A with Dollar Tree looking to divest some Family Dollar stores. In truth there is likely a lot of footprints overlap between the two and consolidation by shutting down underperforming stores is in order.

Finally, folks are starting to question the massive spend on AI related tech. Chamath Palihapitiya has been very vocal about the value proposition of AI chatbots. He further speculates that eventually shareholders will demand a return on their investment from massive spend.

Notes, thoughts and observations - Compiled weekly

I think we all learned an important lesson about stories from journalists who seek to sensationalize topics to generate clicks. The predicted Baltimore supply chain issues never materialized after shipping was shut down by the collapse of the Francis Scott Key Bridge.

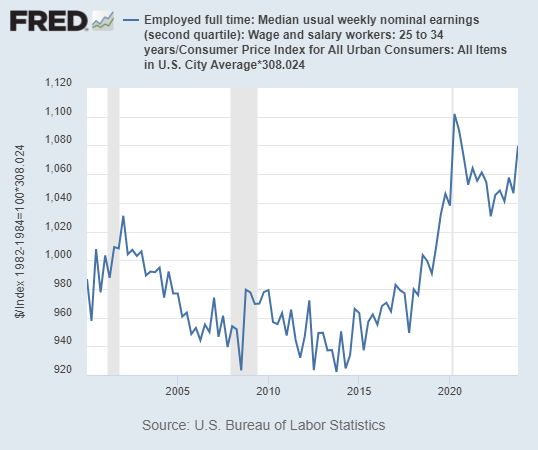

Young workers have the lowest unemployment rate since the 60s and weekly wages are higher than in the past. Again, this contradicts the prevailing narrative that Gen Z is doing worse than previous generations. Look past the commentary at the data.

Median weekly earnings, inflation-adjusted, for young people are the highest they have ever been

Wall Street wasn’t happy with META’s spending on AI. They’d rather the money be returned to the shareholders. We heard a very similar critique with Amazon as Bezos directed online retail profits into building what would become Amazon Web Services. The future of consumer AI will be through service providers, and companies like Meta and Microsoft will play a part.

The idea of natural gas as a bridge fuel is gaining mainstream support with the likes of Jim Cramer admitting as much. I’m still cautious that it will quickly bridge us to nuclear power which is the only reliable base load source that is carbon friendly.

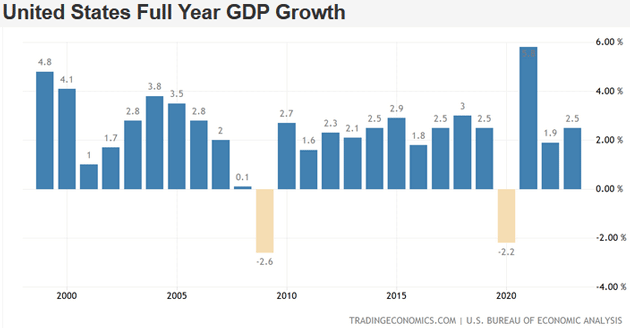

Finally, the economy seems to be roaring ahead despite predictions of current or pending recession. GPD grew steadily but inflation also. Shelter costs and pending trade tariffs will only make inflation stickier. I see daily commentary on how indicators point toward future recession, but I’m mindful that while these indicators have a high correlation the timing is never consistent.

Notes, thoughts and observations - Compiled weekly

Every one that has eye can see that the Fed isn’t cutting interest rates. Apparently the stock market just realized? Bottom line inflation isn’t over and adding tarrifs to steel imports will only add fuel to the fire. Property and insurance is also piliing on inflation pressure

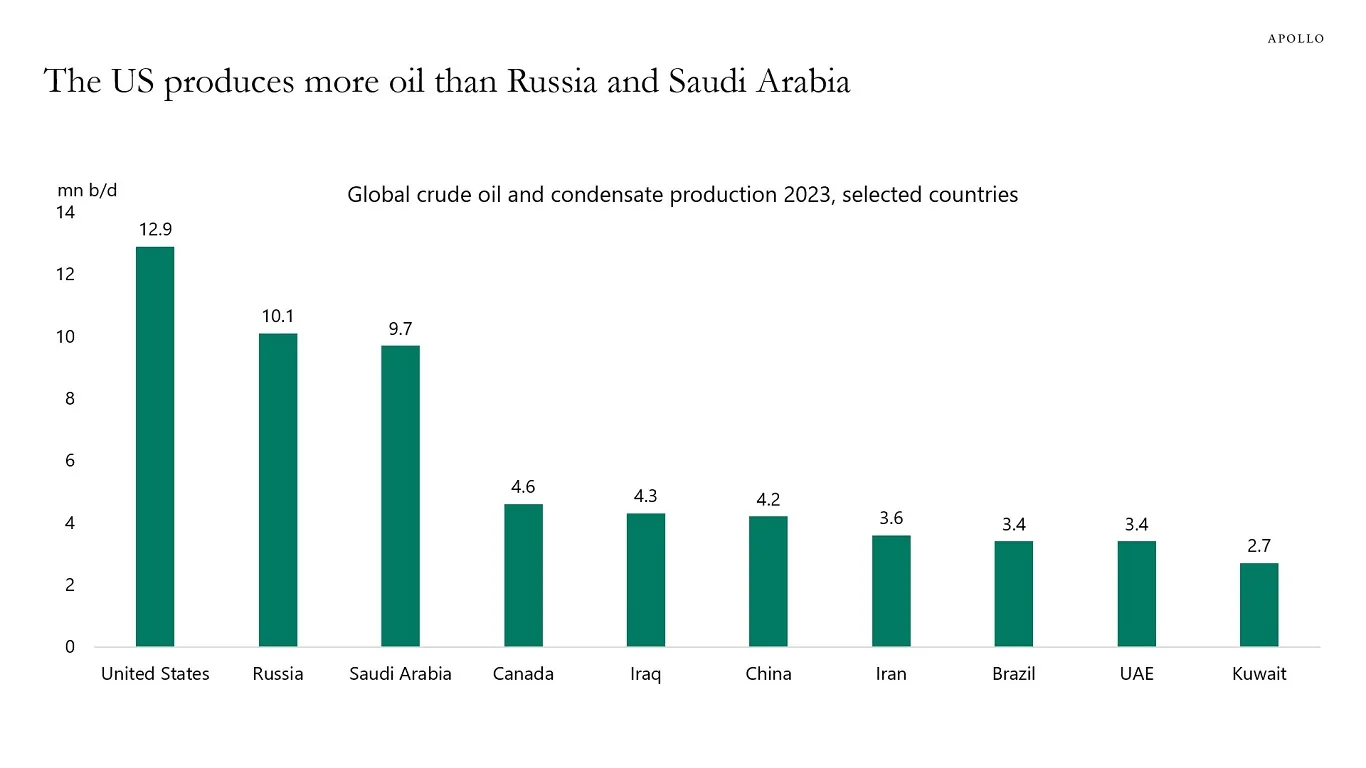

But it isn’t all gloom and doom. Long term energy production will ensure that the US economy remains top dog in the world. We produced a staggering 12.9 million barrels per day in 2023. There is also a broad consensus that natural gas is the right bridge energy to remove the last of the coal fired plants. All of this will remain a tailwind for the US, especially energy intensive industries.

US energy security will fuel future economic growth

The labor market is robust but wage growth has cooled. Long term worker pay needs to stabilize with long term inflation. Inflation is squeezing margins but businesses should expect increasing worker demand for raises. Demographics, increased union support and reshoring will all drive wages.

Elon Musk creates a lot of buzz, but if you look at two of his companies his actual impact is pretty visible. SpaceX has spurred an entire industry of providing cheaper commercial access to space. While success if obvious, the associated cost have not fully worked out. A recent impact of space debris on a home in Florida could become more common and the insurance industry is taking notice. Ultimately who is responsible when a Star Link microsatellite deorbits into someone’s property?

Likewise Tesla has long been the leader in electric cars it he US. Musk’s stated goal was to accelerate the EV technology, and he suceeded. With increasing competition from domestic and foreign manufacturers the company has doubled down on self-driving software side of the business. Again the insurance industry is taking notice. In my opinion, the biggest threat to Musk’s vision is not the technology or the consumers but the regulatory and risk mitigation aspects.

Notes, thoughts and observations - Compiled weekly

Speculation continues on when the next Fed rate move will be, personally I don’t guess. But it’s possible that the source of an interest rate move may come from global forces rather than internal pressure. This hasn’t stopped top CEOs from sharing their opinion. Predict calamity long enough eventually it might become true

Work from home is still to blame for office vacancies, but I’m increasingly thinking that weak business fundamentals are a contributing factor. We are now higher than in 1986 and 1991. Global oil prices are also seeing weakness, though $80 per barrel is priced into the model and seasonal gasoline demand in the US is within historical trends.

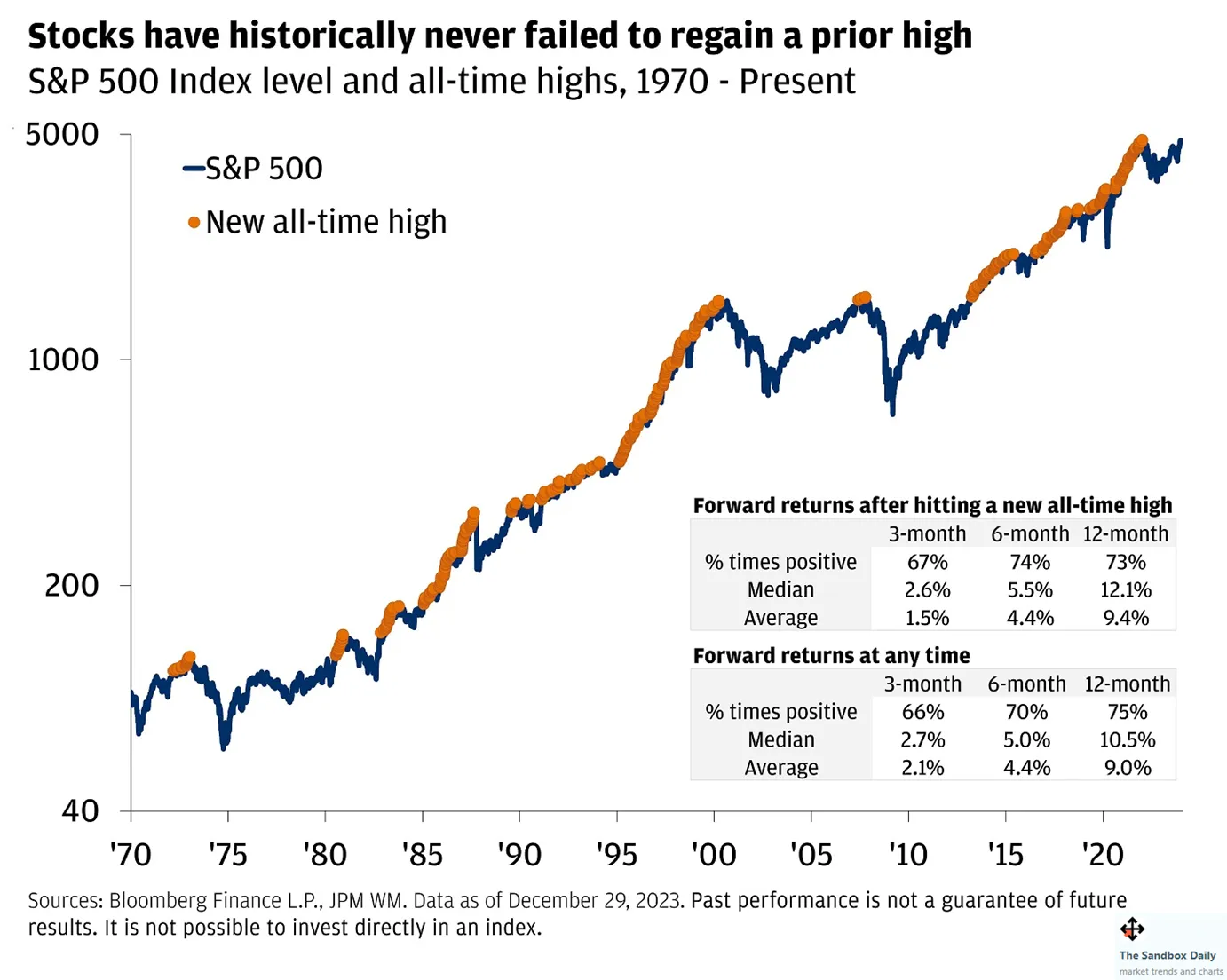

It’s either a stock market bubble or a recession depending on which article you read. Someone pointed out the necessary recovery time for the NASDAQ 100 bought at the peak of the dot com bubble. Sure it took 16 years to recover, but if you held it until today, you’d still be up 276%. Also worth noting that the more diversified S&P 500 only took 7 years to recover.

Fear is ruling the day with folks buying gold from Costco and everyone penning articles about whether we are in a bubble and if it will pop. Sure semiconductors and tech may be VERY overpriced, fundamentals in other sectors could indicate we are on the cusp of a huge expansion in other market areas. Point being diversify and plan for the long-term are a better strategy.

Speaking of semiconductors, it looks like we might be on the verge of a second chip war around purpose-built AI processors. To date Nvidia has leveraged GPU designs but recent announcements by Intel, Meta and Alphabet may create a race to reduce training and inference processing costs. One thing is for certain: current AI processing costs are too high to be sustainable.

Another consideration for AI, EVs and chips is the impact of government incentives, tax breaks and spending programs. These act as fuel for expansion but when they expire it can often cause a rash of business failures. Look no further than the solar industry of the 2000s.

NOTE: Week 15 is a two week combination due to some well deserved time off.

Notes, thoughts and observations - Compiled weekly

The inflation figures weren’t great, but not shocking if you expect a long-term 3-4%.

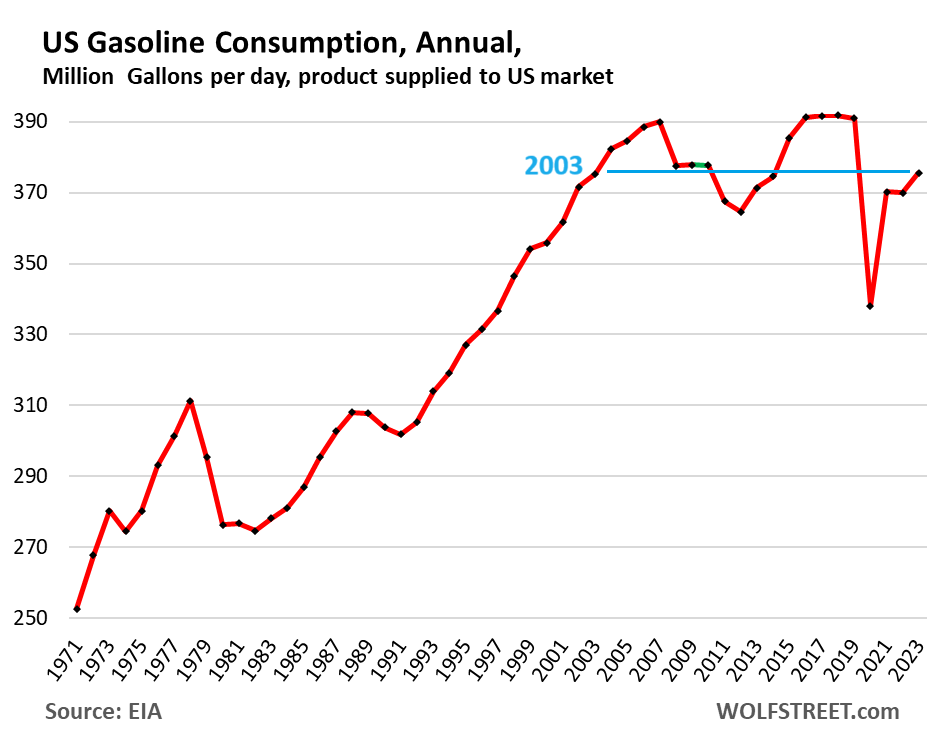

US gasoline consumption is down but EVs aren’t the reason; Average fuel economy is up 42% since 2003. The US produces more oil than any country, ever. Crude oil production in the United States averaged a staggering 12.9 million barrels per day last year.

The Japanese economy appears on the mend after 25 years. Meanwhile strikes paralyze Germany as workers demand higher wages. While employment numbers for white collar workers are weak, blue collar and service workers are still in demand. I’d expect much more union activity everywhere.

3M is looking to follow GE’s lead and spin its health care business. And geopolitical risks are funneling money into the Indo-Pacific region.

Notes, thoughts and observations - Compiled weekly

Job growth in the US continues to be strong, even if it slightly missed expectations. The trades, transportation, construction and utilities all continue to see growth. White collar job losses in professional and business services might make headlines, but otherwise the employment picture is good.

Abroad we are seeing weakness and recession, but the prevailing opinion is that the US will nail a soft landing and avoid outright recession.

Globally energy prices, supply chain disruptions and civil unrest all pull economies in a negative direction. Eygpt is the latest nation to hike interest rates to combat inflation.

Residential real estate continues to be strong, but a recent survey confirmed that rental rates are either flat or declining slightly. This after skyrocketing prices in 2021 and 2022.

One key to the US economic strength is domestic energy production, which stands at an all-time high. In fact, the price is so cheap that production cuts seem likely. Long term this is good as the US will dictate its own energy supply for decades to come.

The stock market tests new highs and that’s not a bad thing. It’s easy to wring your hands about stocks being too expensive but as several articles point out: long term discipline can mitigate the impact of buying at the wrong time.

Not wrong

Finally, the cyber-attack that hit Change Healthcare might have been one of the worst in recent memory. While the victim reportedly paid the ransom, it’s likely that the recovery effort will take a long time. It’s bad, but keep in mind that Change’s parent unit, Optum Insight, only accounts for 12% of parent UnitedHealth’s overall earnings.

Notes, thoughts and observations - Compiled weekly

Rough times for gaming as budgets are slashed and employees let go. Both Sony and Electronic Arts announced major changes. Given the strength of PC and mobile gaming, you must wonder about the future of consoles.

Apple throws in the towel on self-driving cars. Does this signal capitulation that the technology is nowhere close to road ready? Another interesting point is why Apple is reassigning employees from the car division to AI. Is this a FOMO move or was Apple already working on its own AI for vehicles?

Regarding a US recession the data doesn’t indicate that. In fact, many believe there is no imminent danger despite some conflicting metrics. What is a risk is further bankruptcies, like for Macy’s who is closing 150 stores nationwide. The move is due to decadelong underperformance and investors looking for ROI. Things look dark for the retailer if the company can’t pull out of the dive.

The US economy’s statistical vital signs are, if not healthy, at least stable.

The guys on the All-In Podcast had a great discussion about the structure of Nvidia’s business and a breakdown of recent results (worth a watch/listen). A couple of big questions: Are these results based on a sustainable revenue model or are they simply due to a one time build out? Second who spends $22 billion? Big tech companies with lots of cash and not a lot of investment options. But at some point, investors will look for ROI and that could be bad for everyone involved.

Real estate and energy continue to hum along. Home sales are slightly down, but prices are not. It should be noted that long-term inflation accounts for most of the rise in home prices. Meanwhile energy prices remain low in the US because of the shale gas revolution. To quote: “We’ve found almost three Saudi Arabia between oil and natural gas.”

Finally, an interesting tertiary observation about the expansion of AI chips and data centers which generate a lot of heat. Folks are beginning to pay attention to the water usage, for cooling, that these data centers demand. It brings into question the location of data centers in drought-stricken areas, but it also opens the door for alternative cooling technology that Intel and other startups are working on.

Notes, thoughts and observations - Compiled weekly

Tech layoffs have taken the front page as three years of layoffs have far exceeded cuts demanded by simply over hiring. AI is often to blame, but the most likely candidate is the end of zero interest rate policy (ZIRP). Easy money will take time to unwind.

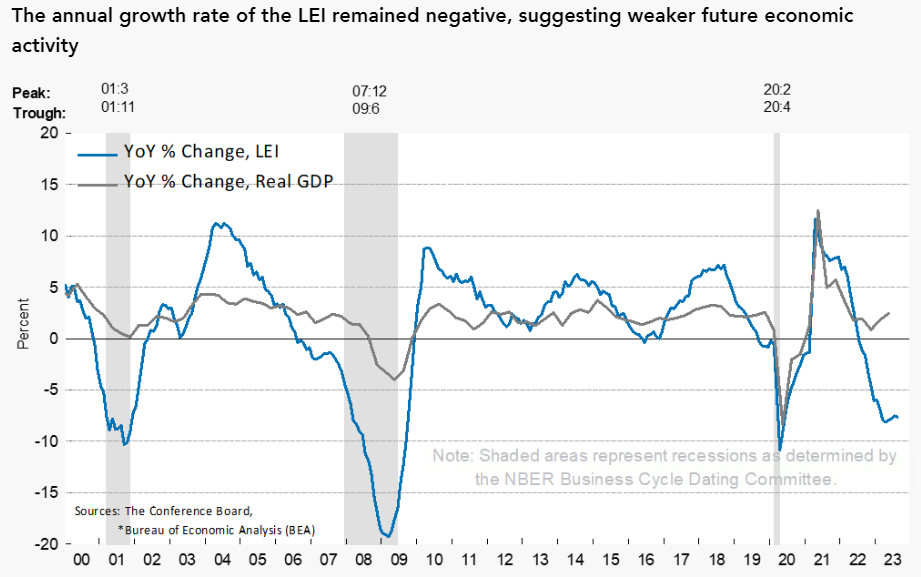

The stock market has already priced in rate cuts, but it is pure fantasy unless the domestic (US) economy takes a dive. Inflation has proven sticky, and analysts warn of a bumpy ride in the short term. However, an economic downturn might be near as coincident indicators point toward recession and consumer credit contracts. Nearly 30% Americans are behind on debt payments.

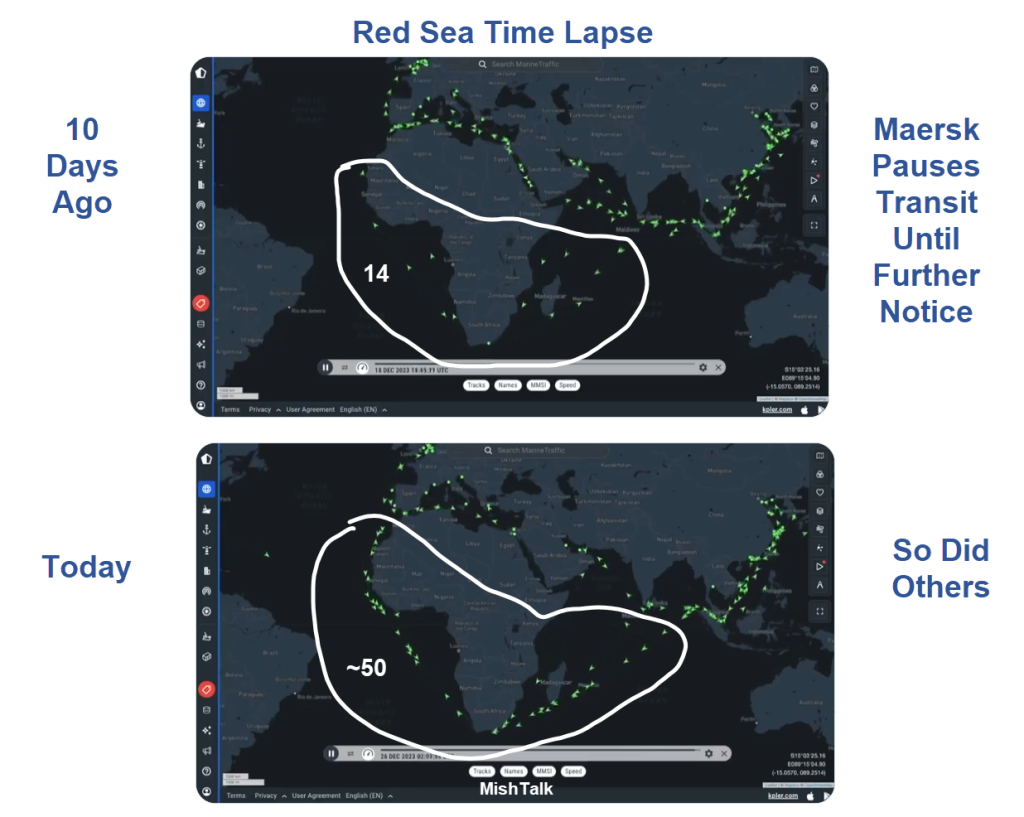

Meanwhile declining demand for oil indicate a global recession and slowing demand from China, and Middle East tensions. Likewise global shipping is under pressure and as it grows more difficult and dangerous, it also grows more expensive. Companies are looking to de-risk, and near shore nations like Mexico offer cheap manufacturing labor.

Red Sea Shipping Update, Maersk Pauses Transit Until Further Notice

Less surprising is the headline that America’s corporate offices are emptier than at any point in at least 4 decades. Remote work, accelerated by the pandemic, has led to a staggering 19.6% of office space in major U.S. cities wasn’t leased. Companies are increasingly interested in smaller, more flexible spaces.

Finally, Gartner recently identified an interesting disruption that you may not have considered. Analysts are predicting a Golden Age of “Silver Workers” due to the talent crunch. The increased experience and productivity of seasoned workers coupled with the democratizes skills via AI could maximize elder workers’ value. The combination of retirement shortfalls and declining worker demographics could make this prediction a reality.

Notes, thoughts and observations - Compiled weekly

This week illustrated the disconnect between big business CEOs and everyone else. Whether it’s Moynihan’s recession denial or Dimon trotting out a classic Warren Buffet trope it’s clear than small and medium size business are seeing a completely different reality.

In the opposing corner we have big box retail on the decline and hard times hitting bottom lines indicating we’re already in recession. Meanwhile everyone is dealing with the painful unwinding of artificially low interest rates. The fed finally paused, but what does it mean?

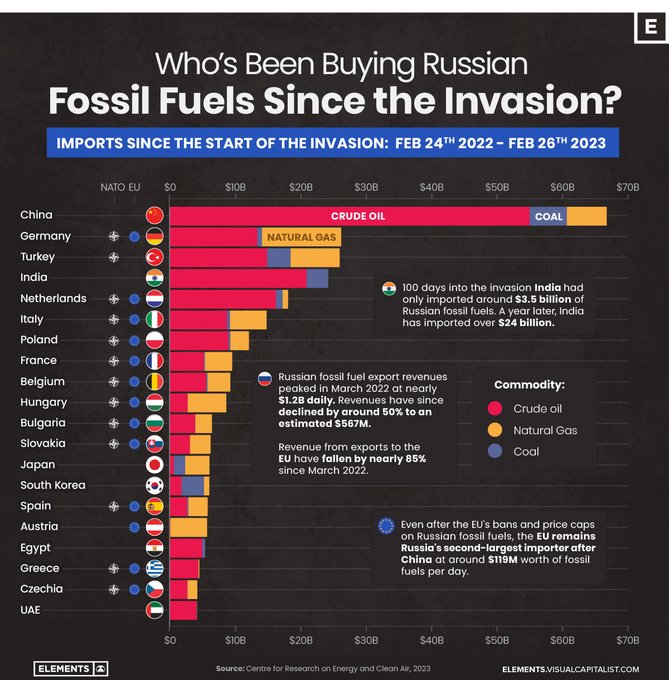

A major force in small business is the push toward profitability. Most everyone knows money is about to get tight and small companies need to get lean. Meanwhile everyone is paying the price of the unprecedented decline in demand during COVID. Organizations like OPEC are still whip-saw trying to deal with fluctuating demand plus the lingering impact of Russian oil embargo.

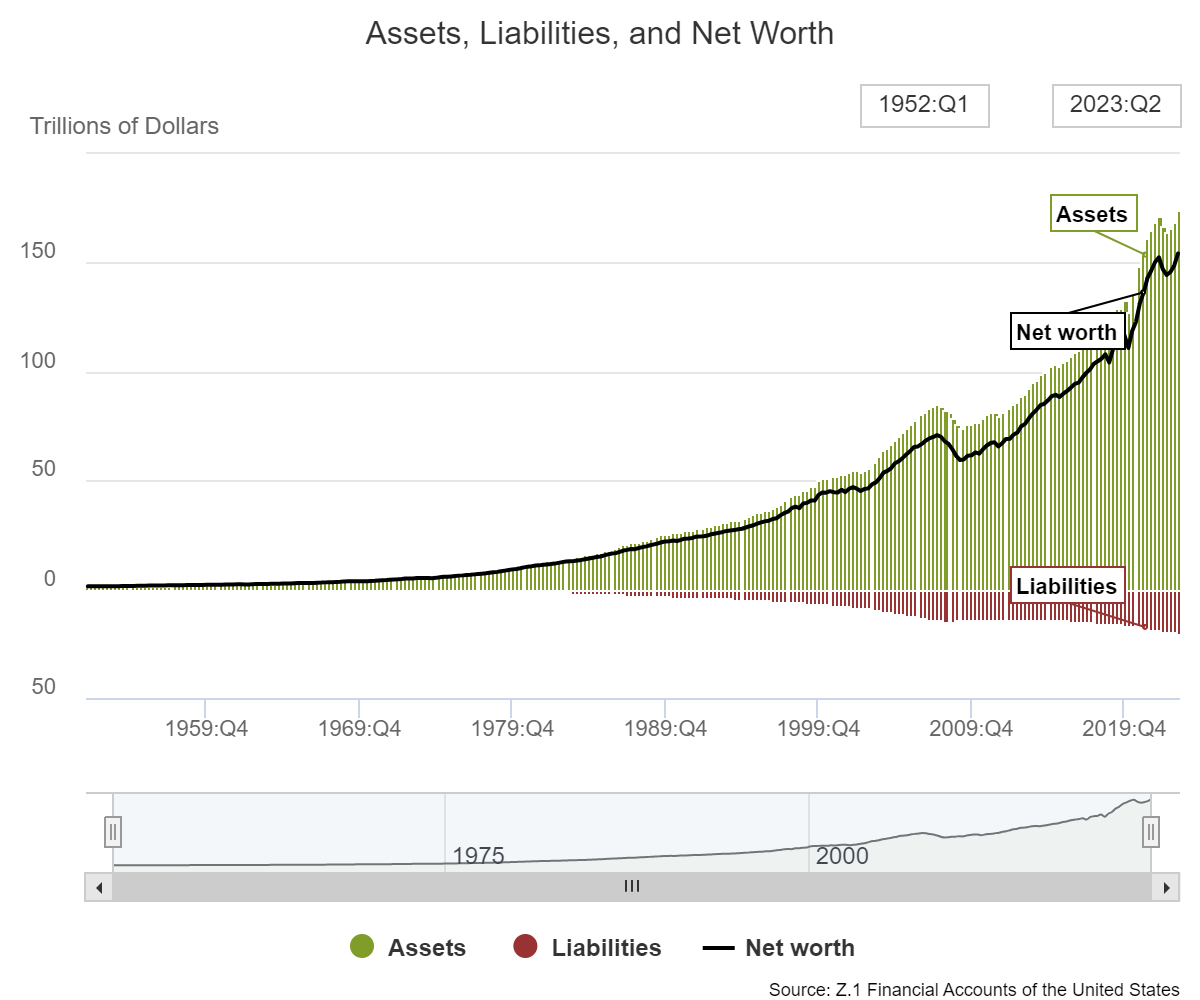

Despite the gloom, at a high level the consumer debt to net worth ratio paints a different picture. Americans are still far better off as net worth climbs faster than debt and that’s good for everyone. On the flip side of high lending rates, the lack of new home construction will continue to prop up residential real estate prices. Supply and demand still alive and well.

Paints a very different picture, net worth is climbing

Notes, thoughts and observations - Compiled weekly

Labor market continues to be tight, in places. Recent wage reports paint a picture of an oversupply of people with college degrees and undersupply of people without.

Inflation remains sticky with everything from drought driving water transport prices to gas prices at $4. It’s also obvious, to everyone except the conference board, that we are IN a recession.

The federal deficit balloons and the solar industry feels the slump of not being proped up by government spending.

Tech IPOs returned with Arm, Instacart and Klaviyo; while the cable industry reaches new lows as CNN has worst ratings weekend on record.

Notes, thoughts and observations - Compiled weekly

More bad news for residential real estate; profitability in focus; national debt balloons; weird energy ideas in UK and sticky gas prices; platform consolidation; econ cycle nears end, what’s next;

The residential real estate market continues to suffer from perceived higher interest rates. Historically not above average, but relatively higher given the long low/no interest rates of recent memory. Housing supply continues to prop up prices which means home sales will certainly slow.

As fundraising and investment has become harder to find companies are now focused on improving profitability. AI companies are not alone, and the once hot tech sector is in the same boat raising prices and cutting costs. This will put pressure on SaaS contracts and employment and belt tightening continues.

The US debt continues to climb and will become prohibitive at some point due to higher interest rates. Meanwhile the UK mulls the idea of natural gas-powered heat pumps which is a weird idea given the Russian embargo and supply shortages. Oil supply tightening will continue to keep fuel prices high

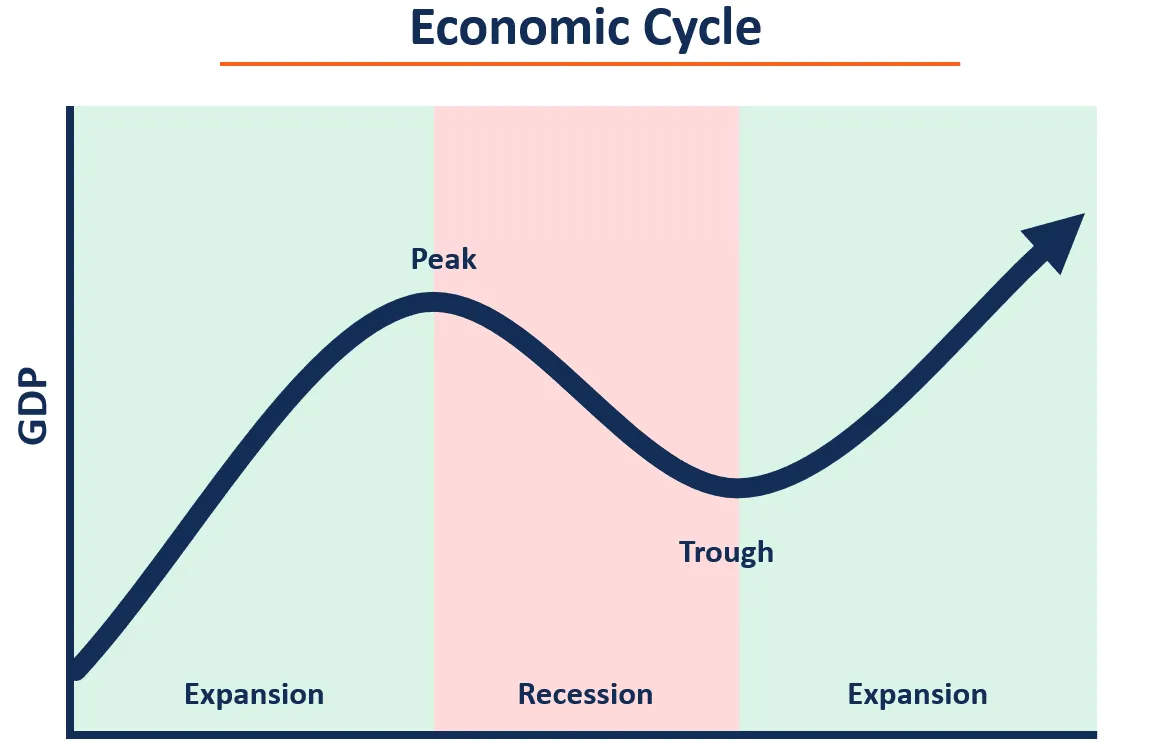

Finally, streaming platforms continue to consolidate as Comcast looks for an exit on Hulu. It is worth noting that Comcast and Disney are still fighting over broadcasting contracts. And is the cycle nearly done? Whether you believe the economy was in recession the historical indicators say we’re nearing the end.

Notes, thoughts and observations - Compiled weekly

This week marked yet another rate hike by the Fed and predictable market hang wringing. More troubling is the designation that we might not be headed for a recession after all. Meanwhile the alarm bells are still sounding, but are they early or late?

The entire cargo and ground transportation sector is in contraction with freight rates down significantly. Strikes by the Teamsters didn’t help Yellow trucking which has all but confirmed they will shut down. Likewise, consumer demand for EVS has stalled with dealers reporting a record number still on the lot.

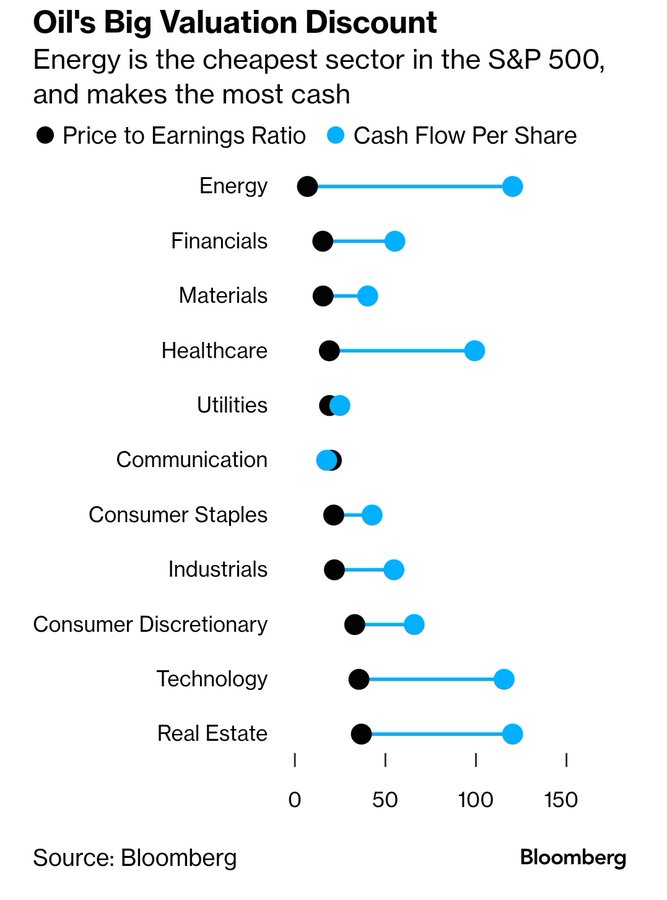

Meanwhile more companies walking away from half-vacant real estate and many market watchers calling a bubble in AI. The most impressive counter view is the value discount for energy stocks particularly oil.

Energy is still vastly underinvested due to ESG hang-over

Notes, thoughts and observations - Compiled weekly

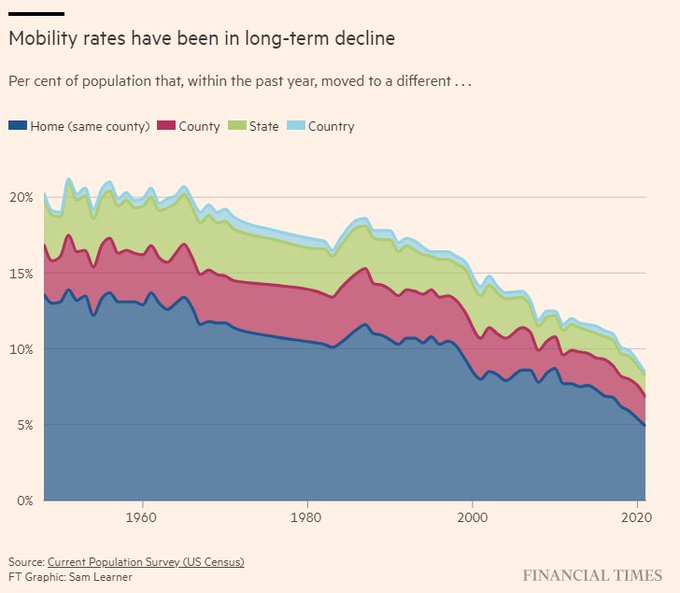

An interesting trend in household mobility due to an interest rate driven and still stalled real estate market. Contraditions abound between an inverted yield curve and a surging S&P 500. But the greatest contradiction is in the acceleration of fossil fuels as emerging economies ramp up energy needs.

Notes, thoughts and observations - Compiled weekly

Concerns abound and uncertainty is high, but one thing is certain we will not return to 2018 levels of any time soon. Banks are getting the double-whammy because of commercial real estate and continued deposit outflows. Spin it how you’d like, but this will bring more banking sector pain.

On the recession front, consumer credit continues to deteriorate, trucking is struggling and and consumer “revenge spending” is expected to peter out by fall. On the other hand the economy is way better than doomsters like to admit and the markets are placing bets on a quick recovery.

Either way fear, uncertainty and doubt abound. Sounds like a great time to shop for names that don’t show up on CNBC or Twitter. 😉

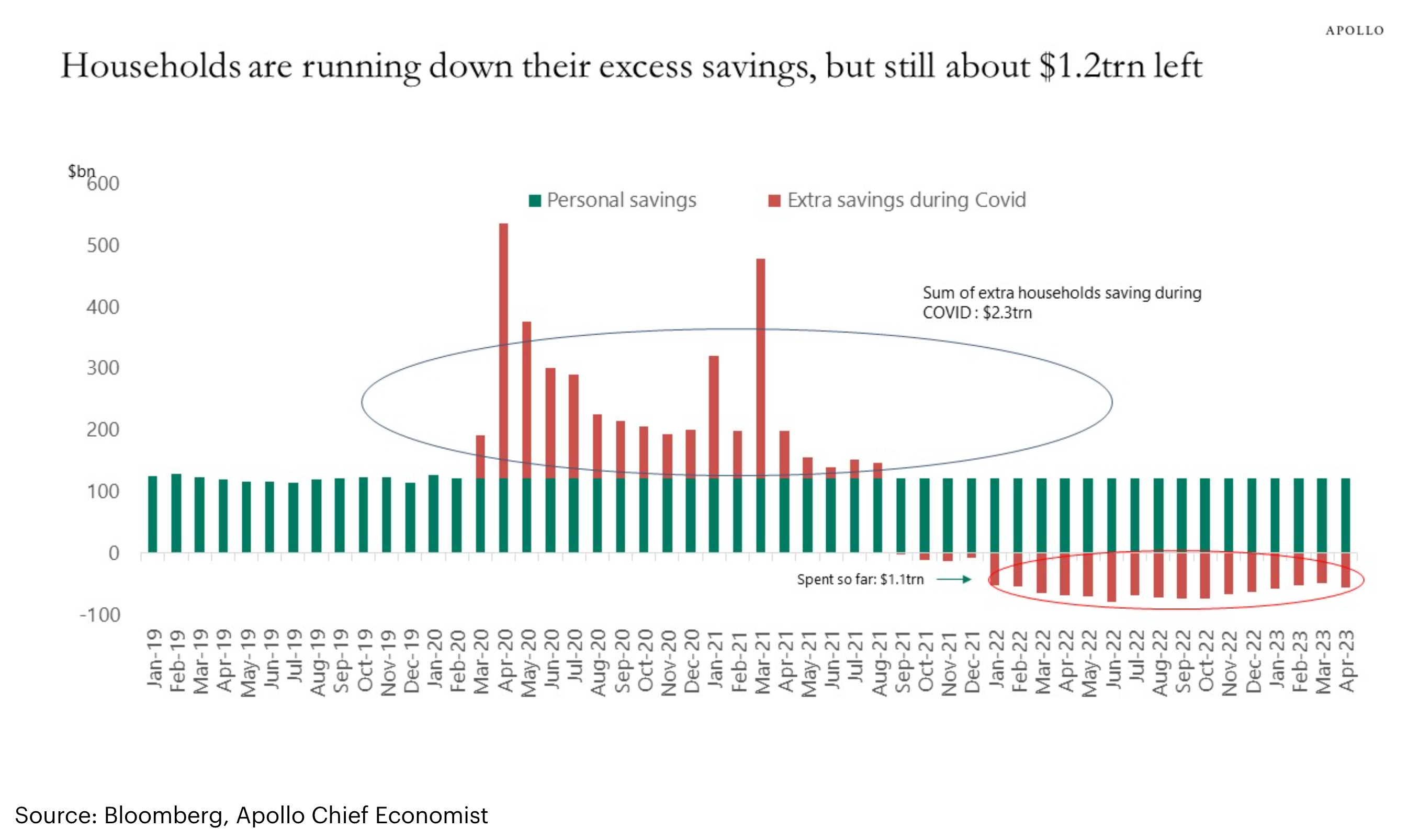

Households are still sitting on $1.2 trillion in excess savings.

Notes, thoughts and observations - Compiled weekly

Another weird week with sources debating a current recession vs other sources predicting the next recession. Not much to say aside from the next few years will be tumultous for the stock market.

Notes, thoughts and observations - Compiled weekly

The labor market looks weird with tech already well through massive layoffs, and job losses spilling over into other sectors with massive layoffs in already weak retail names.

While the energy industry works on renewables and synthetic fuels, bridge energy sources like natural gas are showing promise. While US based natural gas is beholden to regulation, developing regions in Mexico and South America are starting to pop up on the radar.

Rounding out the field we have somewhat of a pullback in real estate, but not the cataclysmic 2008 scenario some had predicted. Low inventory and higher mortgage rates will work against younger millennials.

Millennial homeownership rates badly trail other generations

Notes, thoughts and observations - Compiled weekly

Continued questions and fall out from the bank liquidity bailouts. The market is rattled and there is enough FUD in the system that between credit and consumer pull back there is no way we can avoid a contraction.

That said, I think we are well on our way through this cycle and as historically the designation of a recession comes AFTER the event. Bottom line we are further through this contraction than we think.

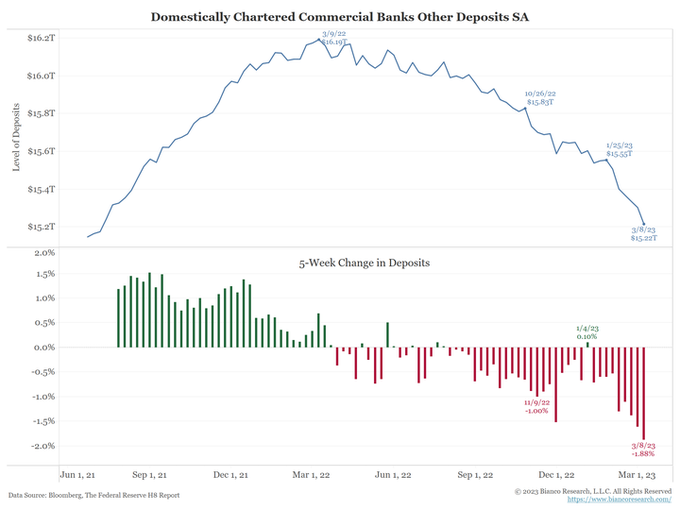

Notes, thoughts and observations - Compiled weekly

Fallout from SVB, Credit Suisse and First Republic and the liquidity crisis. This is far from over, and may result in bailouts.

As I wrote about in Dot-Com Bubble 2.0 we are now entering phase 2 of the downturn when the broader market will reel from tech excesses. I did not anticipate that small regional banks, which lend to small business, could be the catalyst.

My other eye is on energy prices with two things in play. First oil prices are declining which is indicative of a recession but conceals the underlying supply shortage. The second are expiring subsidies on green energy which could have an impact similar to solar back in the late 2000s.

Zeihan’s worldview offers insights on how global politics impact markets and economic trends, helping industry leaders navigate today’s complex mix of geopolitical risks and opportunities. Expect a forward looking approach on what will drive tomorrow’s headlines, delivered in digestible, accessible and relevant takeaways for audiences of all types.

Notes, thoughts and observations - Compiled weekly

Much of this week’s notes are from Mauldin Economic’s Global Macro Update interview with Felix Zulauf. It’s a lot of content and I tried to summarize, but I recommend you watch the original video and check my math.