2024 Week 15

Notes, thoughts and observations - Compiled weekly

Speculation continues on when the next Fed rate move will be, personally I don’t guess. But it’s possible that the source of an interest rate move may come from global forces rather than internal pressure. This hasn’t stopped top CEOs from sharing their opinion. Predict calamity long enough eventually it might become true

Work from home is still to blame for office vacancies, but I’m increasingly thinking that weak business fundamentals are a contributing factor. We are now higher than in 1986 and 1991. Global oil prices are also seeing weakness, though $80 per barrel is priced into the model and seasonal gasoline demand in the US is within historical trends.

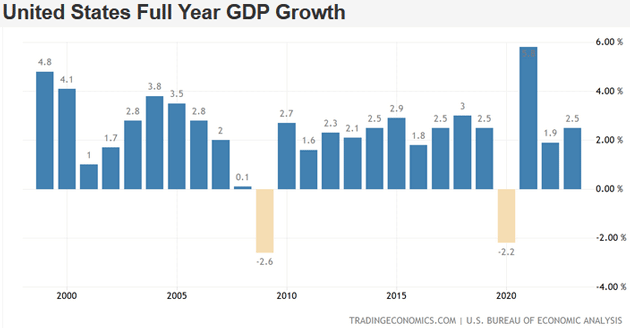

It’s either a stock market bubble or a recession depending on which article you read. Someone pointed out the necessary recovery time for the NASDAQ 100 bought at the peak of the dot com bubble. Sure it took 16 years to recover, but if you held it until today, you’d still be up 276%. Also worth noting that the more diversified S&P 500 only took 7 years to recover.

Fear is ruling the day with folks buying gold from Costco and everyone penning articles about whether we are in a bubble and if it will pop. Sure semiconductors and tech may be VERY overpriced, fundamentals in other sectors could indicate we are on the cusp of a huge expansion in other market areas. Point being diversify and plan for the long-term are a better strategy.

Speaking of semiconductors, it looks like we might be on the verge of a second chip war around purpose-built AI processors. To date Nvidia has leveraged GPU designs but recent announcements by Intel, Meta and Alphabet may create a race to reduce training and inference processing costs. One thing is for certain: current AI processing costs are too high to be sustainable.

Another consideration for AI, EVs and chips is the impact of government incentives, tax breaks and spending programs. These act as fuel for expansion but when they expire it can often cause a rash of business failures. Look no further than the solar industry of the 2000s.

NOTE: Week 15 is a two week combination due to some well deserved time off.

TOPICS

- Fed Rate

- Commercial Real Estate

- Energy

- Stock Market Bubble

- Domestic Recession

- Consumer Credit Crunch

- Labor Market

- Automotive

- Domestic Semiconductor

- Deleverage Globalization

- AI and ML

- EV Battery Technology