Notes, thoughts and observations - Compiled weekly

A combine notes because of time off an holidays

Big themes around the direction of the economy, the labor market and the Fed’s next move. As Keith Fitz Gerald notes: “Trying to anticipate the Fed is a fool’s errand.”

Inflation is close to target, but the Eurozone is clearly in the throes of deindustrialization. Regardless of monetary movements in other countries, US data and corporate results continue to surprise to the downside. Is something big coming, or is it simply a bump in the road?

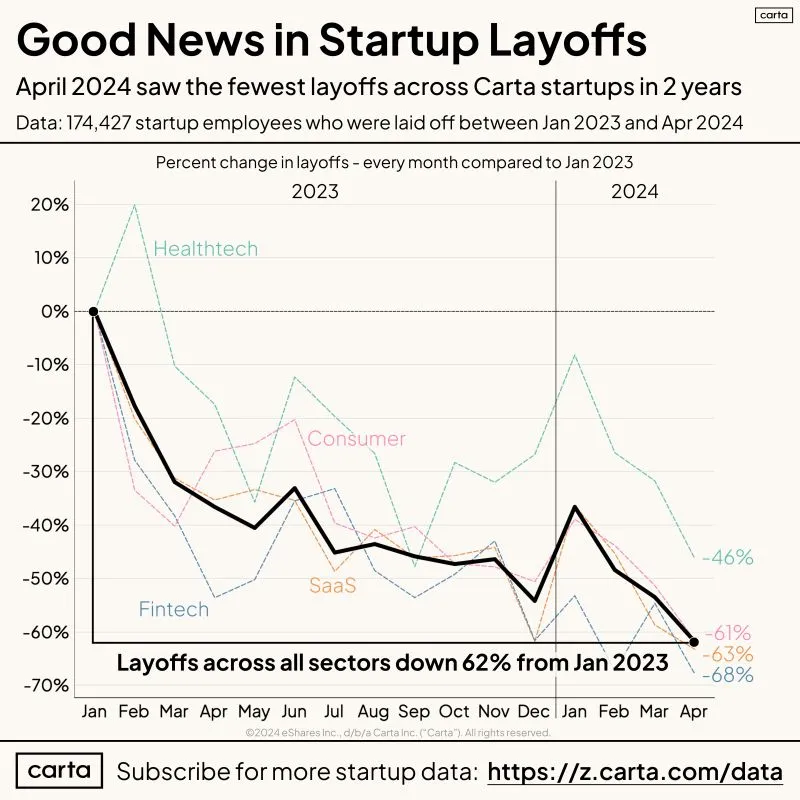

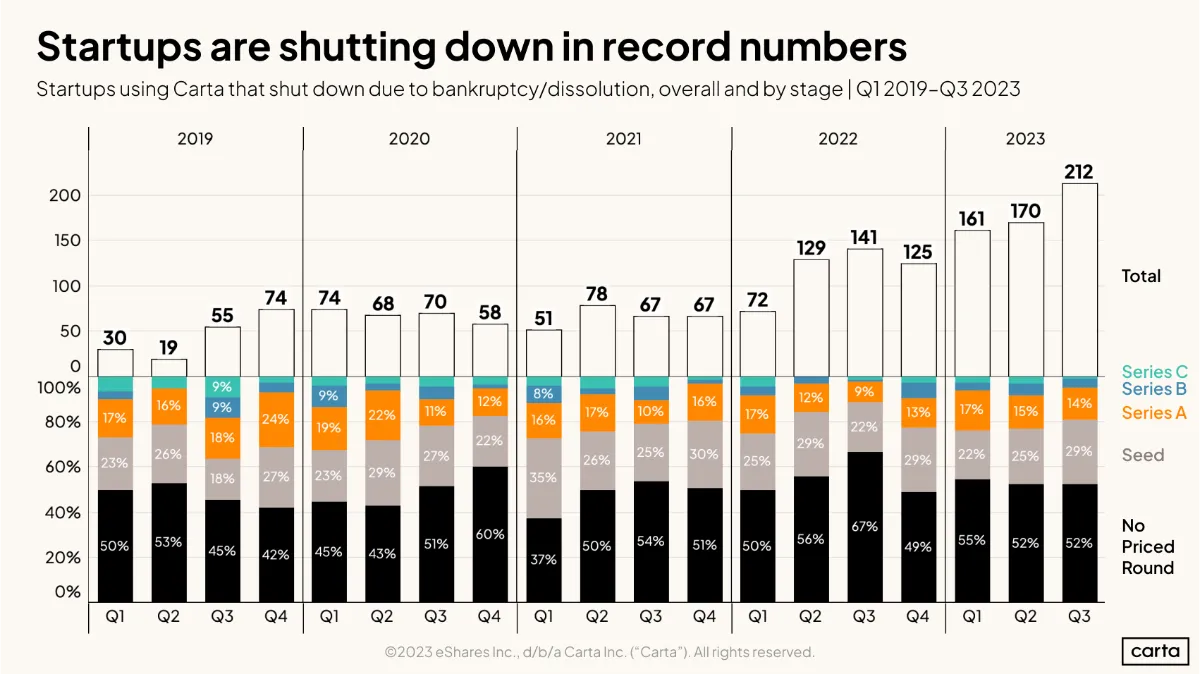

Labor market headlines are often worse than reality. While we’ve reached a high point, since 2021, the rate is still historically low. The expansion is slowing but we aren’t seeing a crash like in 2008. On the flip side, startup layoffs are down 62% since January 2023 per Carta. It’s been steady since early 2022 and may be ending.

Darkest days for startups coming to a close?

The rest of the economy is going through the cycle. Weak companies continue to seek acquisition, or bankruptcy. Financial companies might be in a weakened position but in the near term the 2008 regulations are doing their job.

The biggest headwinds for the economy are the commercial real estate market that has a 20.1% vacancy rate, not seen since the 80s. No indication of how or when this will impact real estate, finance or local governments. Another headwind is the increasing damage from cyberattacks, which impact company bottom lines. However, it’s also an opportunity for companies like Micrsoft to benefit from increased security spending.

Notes, thoughts and observations - Compiled weekly

Growth is slowing around the globe and central banks in Canada, Australia and the Eurozone are signaling rate increases. At some point that will bleed over into the US.

Union pressure ramps up at Amazon as ALU partners with the Teamsters. Hands on labor is still in demand even though office work has been in recession for over a year.

EVs continue to drag down automotive sales and a used car price correction is underway.

The real estate market is still hot, but inventories are starting to recover to pre-pandemic levels. This will create downward pressure on prices but don’t expect a major correction. The real relief will come from more starter homes being built.

A different kind of M&A with Dollar Tree looking to divest some Family Dollar stores. In truth there is likely a lot of footprints overlap between the two and consolidation by shutting down underperforming stores is in order.

Finally, folks are starting to question the massive spend on AI related tech. Chamath Palihapitiya has been very vocal about the value proposition of AI chatbots. He further speculates that eventually shareholders will demand a return on their investment from massive spend.

Notes, thoughts and observations - Compiled weekly

Global pressure once again calls into question the possibility of a Fed rate cut. Either way the world is seeing the demographic decline play out in Japan and need to take heed of their own issues.

Canceling student debt might have mixed popularity, but it’s hard to ignore the economic impact of freeing prime age consumers from the shackles of debt payments. Will it have an impact, hard to say? Again, either way the real reform needs to focus on the cost of college.

Companies are still trying to figure out how to goose results to please Wall Street. Disney, once again under Bob Iger, is reducing head count and refocusing on major box office releases rather than streaming platform releases. Seems like a solid strategy, short term, but long-term Disney faces a lot of challenges.

Meanwhile DuPont is following in the footsteps of GE and others by planning to break up its business units into multiple stand-alone businesses. While it’s easy to imagine that DuPont wants to divest from slower growing business, the reality is likely that each business will focus on the metrics that Wall Street cares about to maximize stock prices.

Notes, thoughts and observations - Compiled weekly

Long term thinking is the only low stress way to invest in the market, and not worry about what the Fed will do. Don’t worry about meme stonks.

Digital media remains in a state of consolidation. Comcast will partner with Peacock, Netflix, and Apple TV to offer bundles. Meanwhile Disney and Warner Bros announced a joint streaming service combining Disney+, Hulu, and Max. Either way the consolidation is starting to make streaming look more like linear TV.

Red Lobster is rumored to be going bankrupt and Under Armour is on the ropes. Corporate debt is less of a concern as businesses adjust to higher interest rates. Consumers, on the other hand, are taking out more debt. But looking beneath the numbers and debt has less to do with consumer spending. Income and wages are far more important.

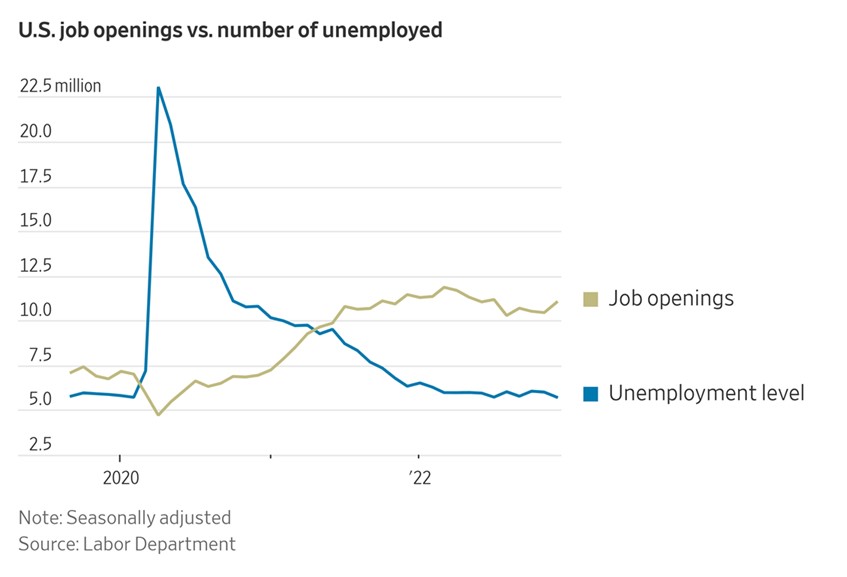

Labor market may be getting less tight

The labor market continues to struggle and we’re seeing layoffs outside of tech. We are also seeing an increase in unionization efforts which will make the southern US more expensive for manufacturing. Demand is high and with or without unions wages are likely to go up, and that will drive inflation.

Notes, thoughts and observations - Compiled weekly

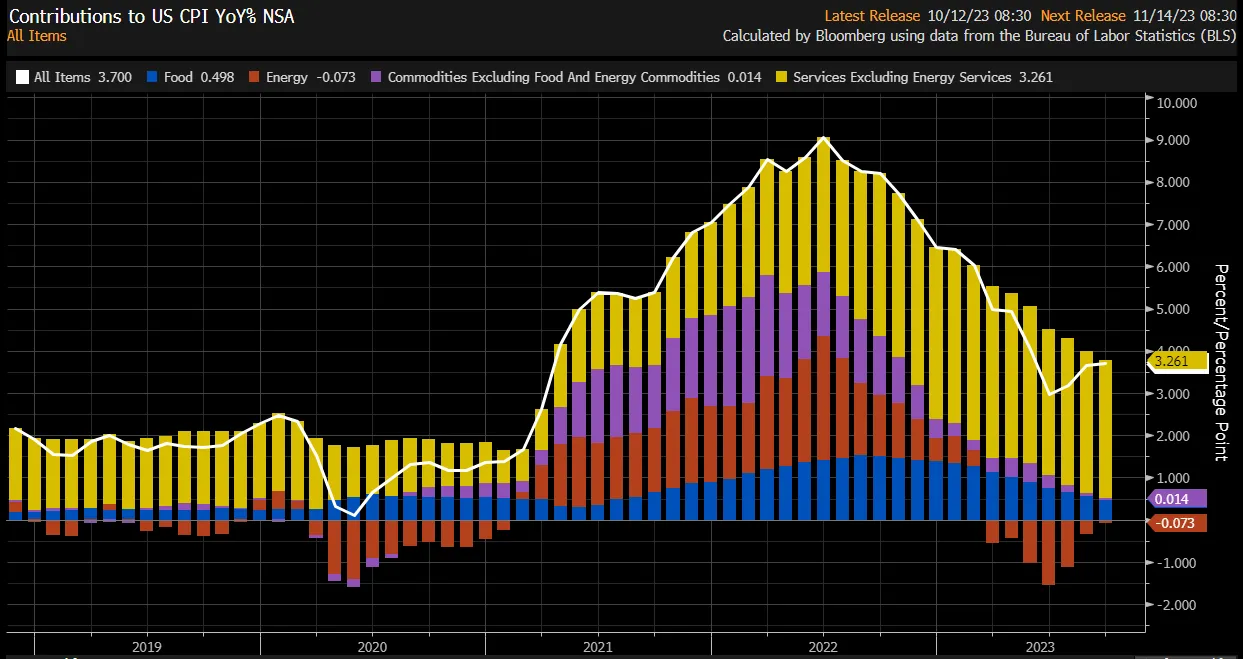

Every one that has eye can see that the Fed isn’t cutting interest rates. Apparently the stock market just realized? Bottom line inflation isn’t over and adding tarrifs to steel imports will only add fuel to the fire. Property and insurance is also piliing on inflation pressure

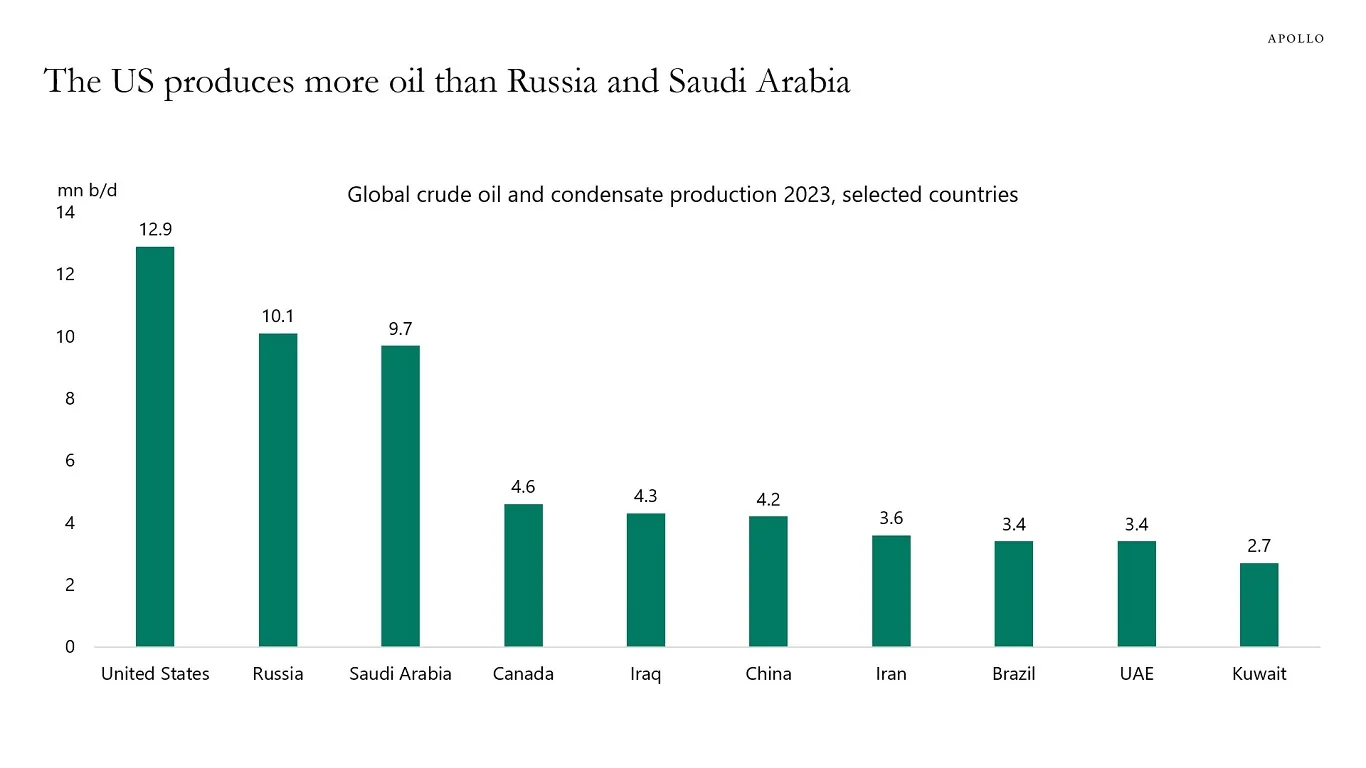

But it isn’t all gloom and doom. Long term energy production will ensure that the US economy remains top dog in the world. We produced a staggering 12.9 million barrels per day in 2023. There is also a broad consensus that natural gas is the right bridge energy to remove the last of the coal fired plants. All of this will remain a tailwind for the US, especially energy intensive industries.

US energy security will fuel future economic growth

The labor market is robust but wage growth has cooled. Long term worker pay needs to stabilize with long term inflation. Inflation is squeezing margins but businesses should expect increasing worker demand for raises. Demographics, increased union support and reshoring will all drive wages.

Elon Musk creates a lot of buzz, but if you look at two of his companies his actual impact is pretty visible. SpaceX has spurred an entire industry of providing cheaper commercial access to space. While success if obvious, the associated cost have not fully worked out. A recent impact of space debris on a home in Florida could become more common and the insurance industry is taking notice. Ultimately who is responsible when a Star Link microsatellite deorbits into someone’s property?

Likewise Tesla has long been the leader in electric cars it he US. Musk’s stated goal was to accelerate the EV technology, and he suceeded. With increasing competition from domestic and foreign manufacturers the company has doubled down on self-driving software side of the business. Again the insurance industry is taking notice. In my opinion, the biggest threat to Musk’s vision is not the technology or the consumers but the regulatory and risk mitigation aspects.

Notes, thoughts and observations - Compiled weekly

Speculation continues on when the next Fed rate move will be, personally I don’t guess. But it’s possible that the source of an interest rate move may come from global forces rather than internal pressure. This hasn’t stopped top CEOs from sharing their opinion. Predict calamity long enough eventually it might become true

Work from home is still to blame for office vacancies, but I’m increasingly thinking that weak business fundamentals are a contributing factor. We are now higher than in 1986 and 1991. Global oil prices are also seeing weakness, though $80 per barrel is priced into the model and seasonal gasoline demand in the US is within historical trends.

It’s either a stock market bubble or a recession depending on which article you read. Someone pointed out the necessary recovery time for the NASDAQ 100 bought at the peak of the dot com bubble. Sure it took 16 years to recover, but if you held it until today, you’d still be up 276%. Also worth noting that the more diversified S&P 500 only took 7 years to recover.

Fear is ruling the day with folks buying gold from Costco and everyone penning articles about whether we are in a bubble and if it will pop. Sure semiconductors and tech may be VERY overpriced, fundamentals in other sectors could indicate we are on the cusp of a huge expansion in other market areas. Point being diversify and plan for the long-term are a better strategy.

Speaking of semiconductors, it looks like we might be on the verge of a second chip war around purpose-built AI processors. To date Nvidia has leveraged GPU designs but recent announcements by Intel, Meta and Alphabet may create a race to reduce training and inference processing costs. One thing is for certain: current AI processing costs are too high to be sustainable.

Another consideration for AI, EVs and chips is the impact of government incentives, tax breaks and spending programs. These act as fuel for expansion but when they expire it can often cause a rash of business failures. Look no further than the solar industry of the 2000s.

NOTE: Week 15 is a two week combination due to some well deserved time off.

Notes, thoughts and observations - Compiled weekly

Bill Gross is predicting that the yield curve needs to flatten, otherwise the long-term outlook for the economy is not positive. Infact everyone is perplexed by the continued inversion of the yield curve. As Howard Marks says “Being too far ahead of your time is indistinguishable from being wrong”

Fisker is on the road to bankruptcy as the company is delisted from the NYSE and its stock price is going to zero. The outlook for EV manufacturers is consolidation and clearly Tesla and BYD are the winners. Speaking of BYD, I can’t imagine a scenario where BYD is allowed to sell vehicles in the US based on security concerns. Given recent revelations of auto manufacturers selling driver data and the political wrangling around TikTok this isn’t going to happen.

Notes, thoughts and observations - Compiled weekly

Where is the stock market going? If the yield curve and consumer spending is an indicator we could be headed for a recession. On the other hand, Black Friday card data says that spending may not be as weak as expected and the VIX indicates a new kind of bullishness not seen in a while. On thing is clear, sectors that performed well outperformed the S&P 500 by a significant amount.

Rent or buy? No not talking about a home, but rather machine learning cycles. Companies like Snowflake continue to grow amid high demand for Nvidia chips. Sometimes it makes sense to rent a server rather than rack your own hardware.

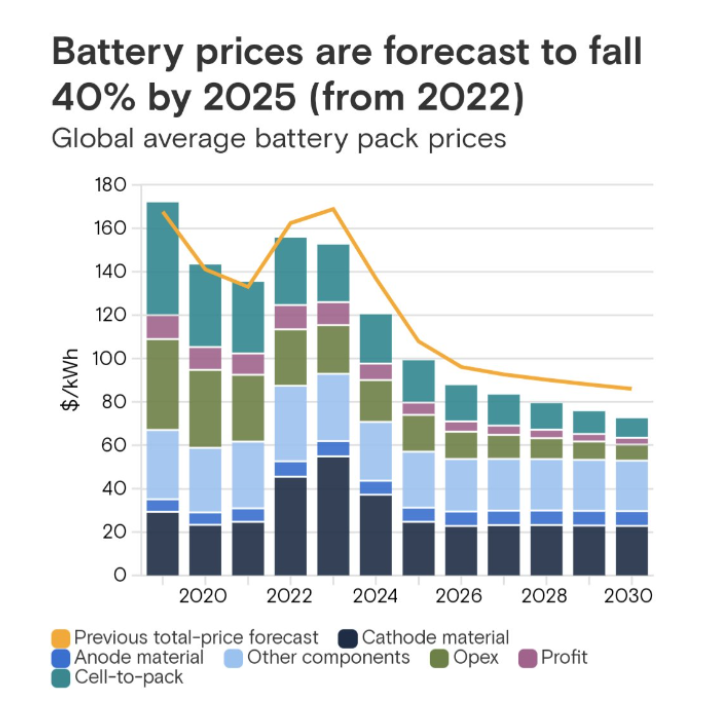

A couple of bright spots. First battery prices are expected to fall and newer technology will improve performance. Likewise, life extending technology like CRISPR gene editing is opening new possibilities in treatment. Finally, even though modular nuclear technology is a non-starter at the moment, the broader application of “hot rocks making steam” is still a benefit to reducing carbon output.

Notes, thoughts and observations - Compiled weekly

A mixed bag of news this week. Inflation remains on the radar, as do future fed hikes. The labor market remains strong but finance continues to shed jobs.

Services remain higher likely to due to higher wages

Notes, thoughts and observations - Compiled weekly

Commercial real estate seems to be stabilizing, while the housing market has gone cold. Meanwhile in China, Country Garden issues a dire warning and has missed loan payments. This could unlock a fresh hell of financial worries.

The speculative bubble in use cars continues to unwind and is shaking out weak companies like Shift Technologies who filed for Chapter 11 this week. Meanwhile Tesla continues to lower prices to both chase higher volumes and to also compete with BYD.

As soon as the Fed stopped raising rates everyone began speculating when rate cuts would begin. Some think higher for longer and others believe that history indicates cuts sooner. Either way a rate cut will be a temporary boost for borrowing. Long term, near-zero rates are gone, and the economy needs to adjust its risk-reward equation.

Profitability and debt reduction among companies is a high priority. Rising rates will ensure that weak and heavily indebted companies meet an end. Likewise high valued scaleups like Airtable need to mind the bottom line and show significant revenue to justify their valuations. All in all, the number of shutdown startups is rising as companies begin running out of money and are unable to raise.

Notes, thoughts and observations - Compiled weekly

Everyone on Wall Street and in finance is worried about the fed rate and when cuts will begin. This largely ignores the real impact that high interest rates (i.e., borrowing cost) have on everyday people.

On one hand the cost for consumers to borrow and maintain their lifestyle amid rising prices is in serious jeopardy. The credit crunch is ongoing and should be a concern to everyone. It has largely propped up buying, as have government transfer payments. Those payments are coming to an end and student loans are coming due.

The flip side of higher interest rates is the inevitable downward pressure on home prices. It’s a matter of affordability for buyers and we are finally starting to see it. Commercial real estate is in a far worse situation, and I think the prediction of a bottom in mid 2024 is optimistic. It less about a bottom in commercial real estate and more about a long term underperformance.

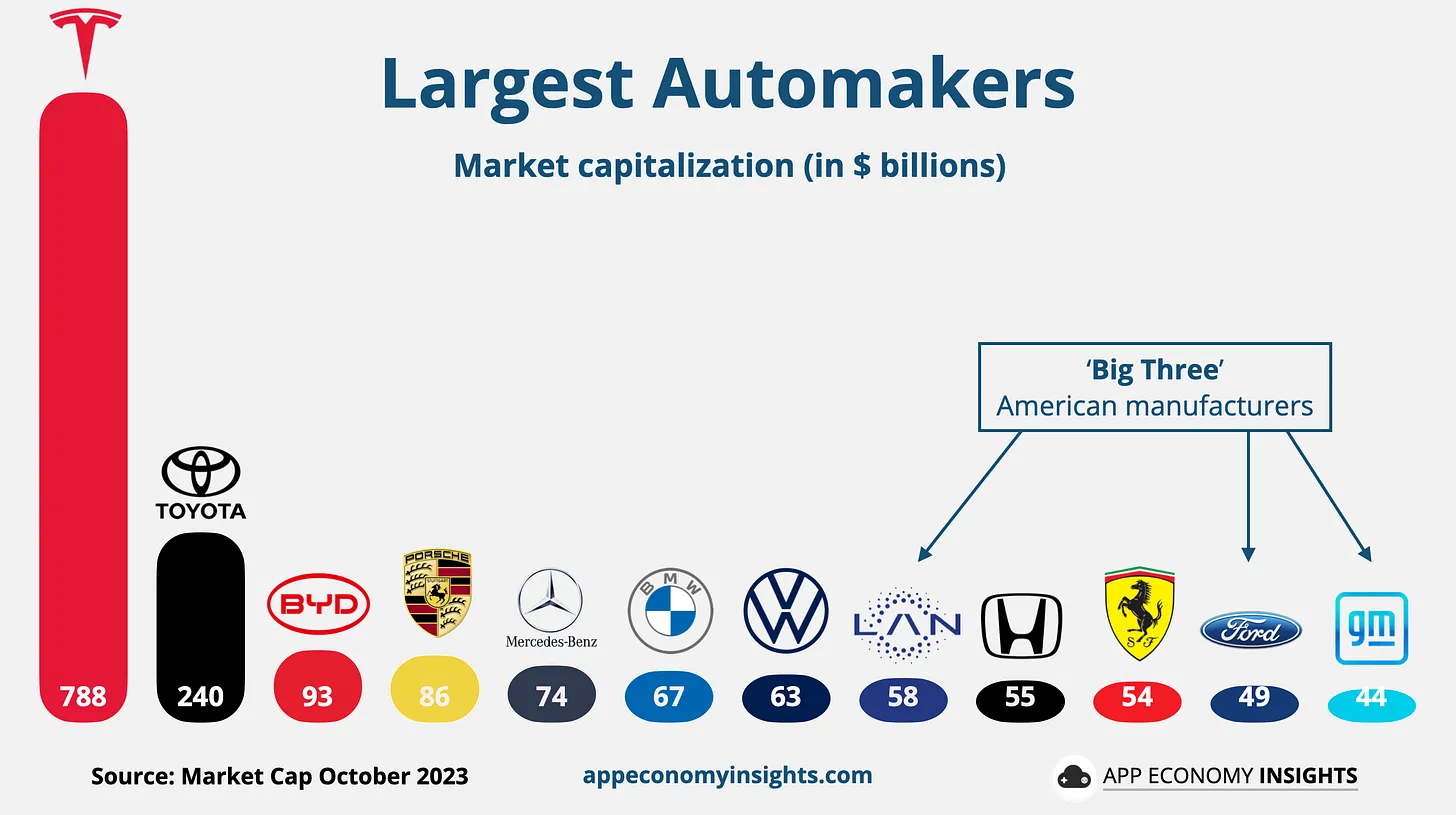

Not surprisingly, the deterioration in household finances is fueling a rise in credit delinquency, particularly in automotive. As if that weren’t enough the big three US auto manufacturers are experiencing worker strikes and more alarming a decline in market cap. Most shocking both Ford and GM have less global market cap than Ferrari which produces a fraction of the number of vehicles.

Top 12 automakers worldwide, ranked by market cap

But notice something else, tucked in between Tesla and BYD is Toyota. Not only does Toyota have the reputation for building reliable internal combustion cars that are a great value, but Toyota has also sold vehicles in the hybrid space for years. The Prius is the bestselling hybrid car of all time first for sale outside of Japan 23 years ago. We should take notice when Toyota recently announced a long-term battery partnership with LG Energy Solution.

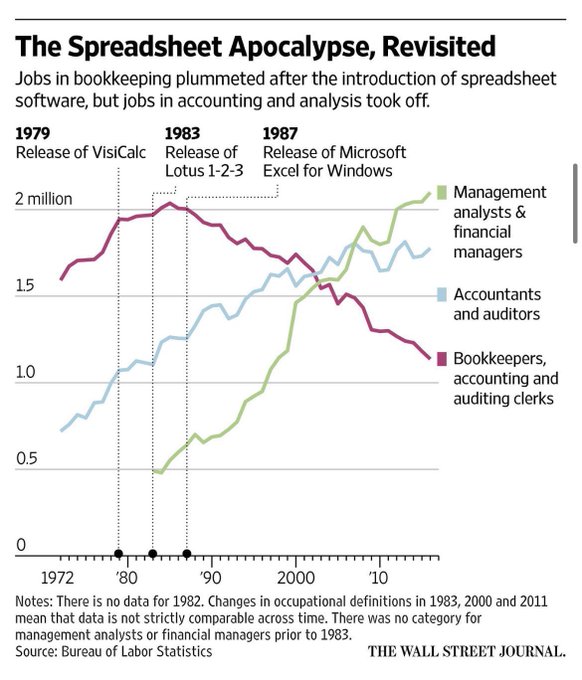

The last point for the week is a great example of how correlation does not imply causation. The spreadsheet did not in fact destroy the bookkeepers job, and it is not an analog of the AI revolution. I know that a lot of finance is done via spreadsheets, but no sizeable business is using Excel to track accounting auditing. There are purpose built systems for that and they are expensive for companies and lucrative for SaaS providers.

Notes, thoughts and observations - Compiled weekly

This week illustrated the disconnect between big business CEOs and everyone else. Whether it’s Moynihan’s recession denial or Dimon trotting out a classic Warren Buffet trope it’s clear than small and medium size business are seeing a completely different reality.

In the opposing corner we have big box retail on the decline and hard times hitting bottom lines indicating we’re already in recession. Meanwhile everyone is dealing with the painful unwinding of artificially low interest rates. The fed finally paused, but what does it mean?

A major force in small business is the push toward profitability. Most everyone knows money is about to get tight and small companies need to get lean. Meanwhile everyone is paying the price of the unprecedented decline in demand during COVID. Organizations like OPEC are still whip-saw trying to deal with fluctuating demand plus the lingering impact of Russian oil embargo.

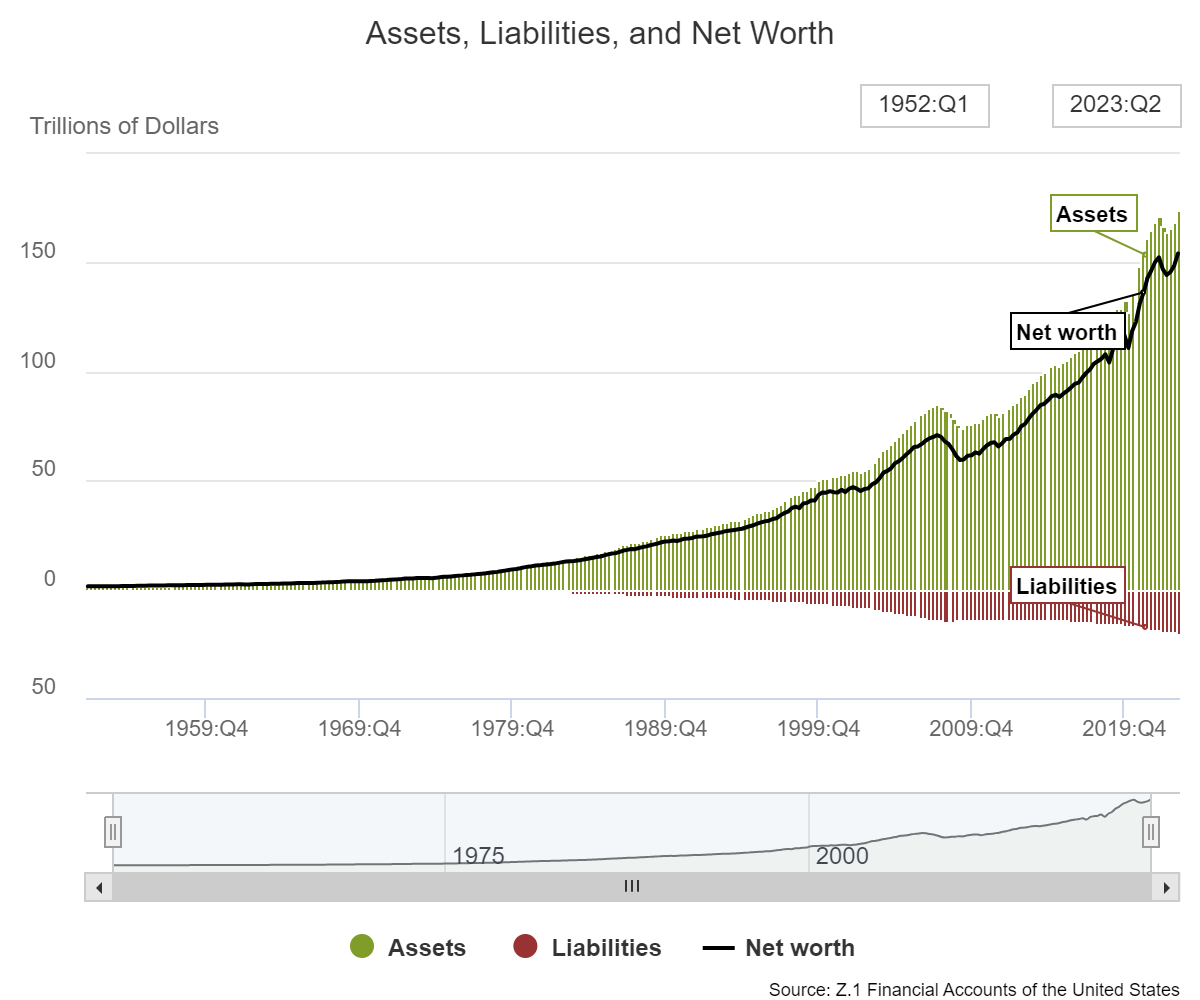

Despite the gloom, at a high level the consumer debt to net worth ratio paints a different picture. Americans are still far better off as net worth climbs faster than debt and that’s good for everyone. On the flip side of high lending rates, the lack of new home construction will continue to prop up residential real estate prices. Supply and demand still alive and well.

Paints a very different picture, net worth is climbing

Notes, thoughts and observations - Compiled weekly

Labor market continues to be tight, in places. Recent wage reports paint a picture of an oversupply of people with college degrees and undersupply of people without.

Inflation remains sticky with everything from drought driving water transport prices to gas prices at $4. It’s also obvious, to everyone except the conference board, that we are IN a recession.

The federal deficit balloons and the solar industry feels the slump of not being proped up by government spending.

Tech IPOs returned with Arm, Instacart and Klaviyo; while the cable industry reaches new lows as CNN has worst ratings weekend on record.

Notes, thoughts and observations - Compiled weekly

This week marked yet another rate hike by the Fed and predictable market hang wringing. More troubling is the designation that we might not be headed for a recession after all. Meanwhile the alarm bells are still sounding, but are they early or late?

The entire cargo and ground transportation sector is in contraction with freight rates down significantly. Strikes by the Teamsters didn’t help Yellow trucking which has all but confirmed they will shut down. Likewise, consumer demand for EVS has stalled with dealers reporting a record number still on the lot.

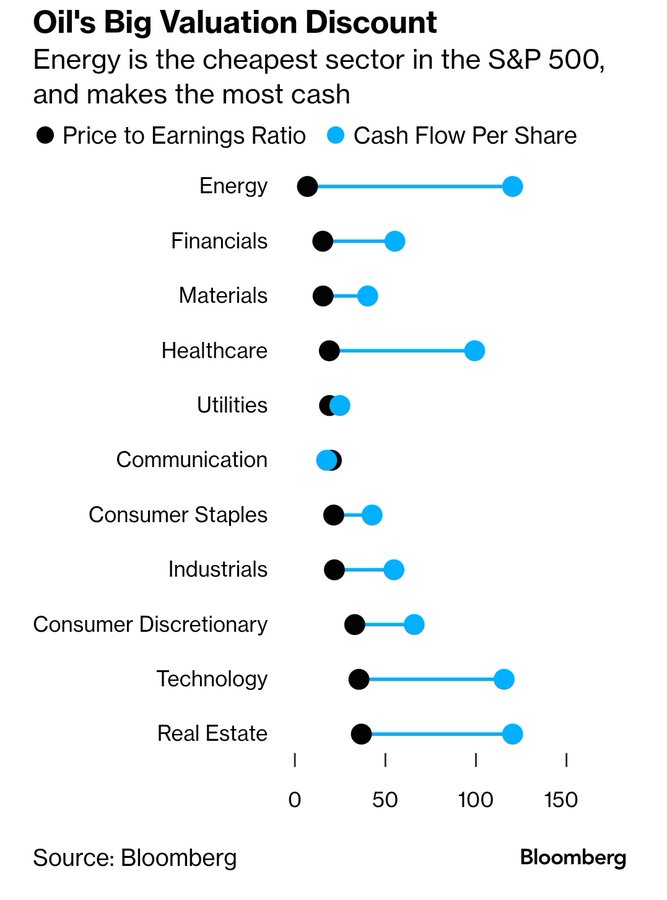

Meanwhile more companies walking away from half-vacant real estate and many market watchers calling a bubble in AI. The most impressive counter view is the value discount for energy stocks particularly oil.

Energy is still vastly underinvested due to ESG hang-over

Notes, thoughts and observations - Compiled weekly

Rolling together two weeks of notes and noticing big trends in real estate, the impact of rising rates and the labor force. Realtor.com reports a record low number of listed homes for sale, which will put upward pressure on prices but also benefits services, home improvement and rental property.

Inflation numbers came in and continue to trend downward, but the consensus is that the Fed will continue to hike rates until it hurts (or YOY inflation goes negative as history indicates). Higher rates won’t make Wall Street happy for long but will have a real impact on both corporate and private debt. The former will impact the earnings bottom line, and the latter in the form of lower consumer spending.

The question everyone is asking “Are we having a recession or not?”. It’s less of “if” than “when” as all eyes fix on the still inverted yield curve. The real question is hard landing or soft landing. A lot of conjecture and uncertainty.

Finally, what does Gen Z want? More precisely, as they enter the workforce, what do they want from the work relationship? Gen X historically wanted to come in, work and go home. Millennials demanded more of their employers. But has Gen Z been in the workforce long enough to know what they truly want?

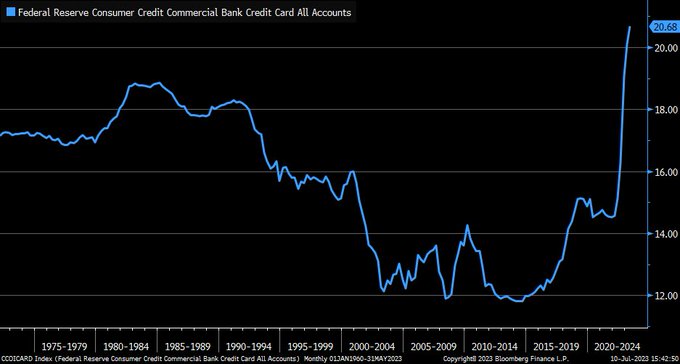

Credit cards issued by commercial banks have interest rates soaring close to 21% as of May, which is a record in Fed data going back to early 1970s

Notes, thoughts and observations - Compiled weekly

A lot of noise this week and not much meaningful signal. Home Depot missed on revenue which indicates consumer weakness. Contrary, private debt continues to climb despite rising insterest rates and the labor market remains sutbornly strong.

Notes, thoughts and observations - Compiled weekly

Weird… big data analytics company Palantir dumps $50 million gold investment and buys $1.62 billion treasuries. What do they know? Gold is typically a hedge against inflation. Treasuries, on the hand, move inverse to interest rates. Is this a prediction of interest rate cuts?

Meanwhile stress on regional banks continues but I’m more confident that it won’t spill into outright contagion. That said I expect more bankruptcies among weaker companies.

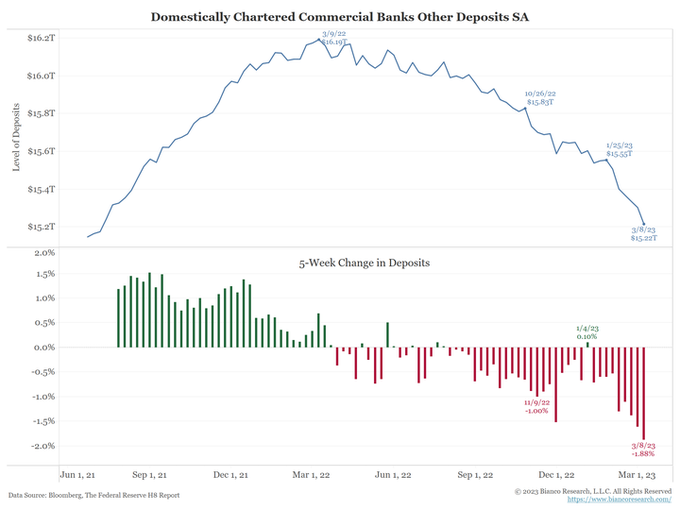

This remains one of the craziest chart pictures in my career… - Michael Green

Notes, thoughts and observations - Compiled weekly

Continued questions and fall out from the bank liquidity bailouts. The market is rattled and there is enough FUD in the system that between credit and consumer pull back there is no way we can avoid a contraction.

That said, I think we are well on our way through this cycle and as historically the designation of a recession comes AFTER the event. Bottom line we are further through this contraction than we think.

Notes, thoughts and observations - Compiled weekly

Fallout from SVB, Credit Suisse and First Republic and the liquidity crisis. This is far from over, and may result in bailouts.

As I wrote about in Dot-Com Bubble 2.0 we are now entering phase 2 of the downturn when the broader market will reel from tech excesses. I did not anticipate that small regional banks, which lend to small business, could be the catalyst.

My other eye is on energy prices with two things in play. First oil prices are declining which is indicative of a recession but conceals the underlying supply shortage. The second are expiring subsidies on green energy which could have an impact similar to solar back in the late 2000s.

Notes, thoughts and observations - Compiled weekly

Much of this week’s notes are from Mauldin Economic’s Global Macro Update interview with Felix Zulauf. It’s a lot of content and I tried to summarize, but I recommend you watch the original video and check my math.